- Market Insights

- 5 mins

Get a deeper understanding on how this development impacts your investing.

Schedule a no-fee, no-commitment consultation with our cross-border advisors.

The S&P 500 index recently closed above 5,000 and set a new all-time high, less than three years after it first crossed the 4,000 mark. While some are understandably nervous any time the market is near record levels, investors also tend to grow more bullish as the momentum continues. Across market cycles, fear often turns to caution, giving way to optimism and eventually irrational exuberance. With the market's rapid climb over the past year, what should investors keep in mind to stay disciplined and focused on their financial plans?

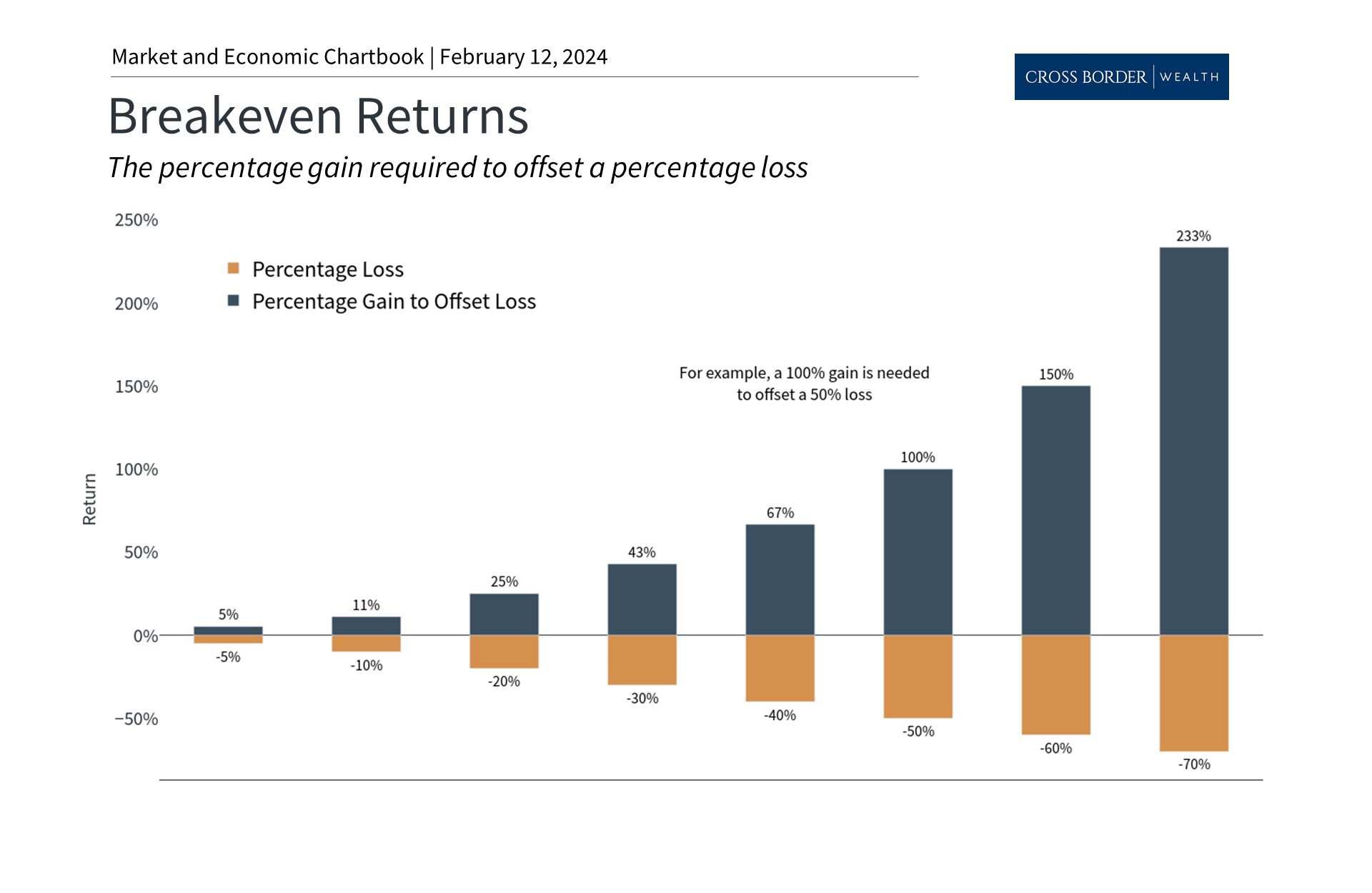

Much larger percentage gains are needed to offset losses

For some investors, it may increasingly feel as if the market can only go up despite ongoing financial and economic uncertainty. The bear market of 2022 may even seem like a distant memory now that the Fed is expected to cut rates and inflation has fallen to more manageable levels. While structuring portfolios to benefit from market gains is important, it's also critical to manage risk. How investors behave when markets are down - even if only for a few days, weeks or months - can be as important as how they position over years and decades. In this context, there are a few key principles to keep in mind.

First, the way investment returns are calculated can create a daunting situation for investors. This is because positive and negative compound returns are not symmetric - in general, a larger gain is needed to offset a loss. For instance, a 10% decline requires an 11.1% gain to recoup those losses. These differences grow with larger percentages, as shown in the accompanying chart. It's easy to see that a 50% decline, which cuts the value of a portfolio in half, would require a 100% increase to return to the original value. The effect of losses on compounded returns is sometimes referred to as a "volatility tax" or "volatility drag."

Thus, in the midst of an inevitable market pullback, it can be easy for investors to become discouraged by the magnitude of the gain needed to return to par. However, history shows that markets do rebound over time, even when the S&P 500 declines nearly 50% as it did in 2008 or 34% as it did in 2020, making up for these losses on their way to new all-time highs. Of course, the timing of these rebounds is difficult if not impossible to predict. Thus, it's important to stay invested and not focus on the magnitude of gains and losses.

Having a smoother ride can help investors stick to their long-term plans

Second, one of the most important ideas in behavioral finance is known as "loss aversion," the idea that losses tend to feel worse to investors than similar gains. A simple example is that finding twenty dollars on the ground will certainly make you happy but accidentally losing a twenty-dollar bill - or having it stolen from you - will likely make you more upset. This asymmetry in how we experience gains and losses grows as the amount increases. In the extreme, large portfolio gains may make investors quite happy for a short time but large losses may lead investors to give up on their financial plans altogether.

While most investors would like to generate significant portfolio gains year in and year out, the reality is that markets are inherently volatile. This is why, from a long-term perspective, it is far more important for investors to build a portfolio and financial plan that they can stick with through good and bad times, rather than a portfolio with the best theoretical returns.

The accompanying chart shows four different asset allocation portfolios and highlights how different their paths have been since the 2008 financial crisis. Clearly, an all-stock portfolio would have performed best over the past 15 years. However, there are few investors who can stomach losses on the order of 50% over the course of years. Thus, most investors would have been better served holding a diversified portfolio instead. Not only would their returns have been quite strong over this period, but they would have been more likely to stick to their financial goals despite the many challenges along the way.

How investors react to bull and bear markets can have long-term

consequences

Finally, the idea that the timing of positive and negative returns matters is known as "sequence of returns risk." In a perfect world, whether an investor experiences a bear market or bull market first would not affect the final outcome, as shown in the dotted lines in the accompanying chart. In reality, however, investors will likely behave differently in bull and bear markets, and they may be withdrawing from their portfolios along the way, creating a drag that is compounded over time. This is yet another reason investors should be careful of making sharp portfolio adjustments during periods of market volatility, and should consult with a trusted advisor on portfolio positioning and withdrawals.