- Market Insights

- 5 mins

Get investing insights for US-connected global citizens.

Book a free consultation with our cross-border advisors.

Financial markets rebounded in May with the S&P 500 recovering its year-to-date losses. This positive month occurred against a backdrop of new trade agreements, mixed economic signals, and ongoing concerns about U.S. fiscal health. While many reports continued to show that the economy is strong, consumers remained pessimistic about the future. Treasury yields fluctuated throughout the month due to concerns around federal spending and debt. For long-term investors, May serves as a reminder that markets can adapt to changing conditions, even when there is significant uncertainty around economic and fiscal policy.

Markets continued to recover despite new concerns

May's market rebound underscores the importance of staying the course during periods of market volatility. After a challenging April, markets demonstrated resilience by recovering most of their losses and returning to positive territory in May. This illustrates how quickly market sentiment can shift when conditions begin to stabilize, a pattern that investors have experienced many times over the past decade. Of course, the past is no guarantee of the future, and markets will continue to worry about trade deals, the U.S. debt, and the health of the economy in the coming months.

Moody's downgraded the U.S. credit rating

Past performance is not indicative of future results

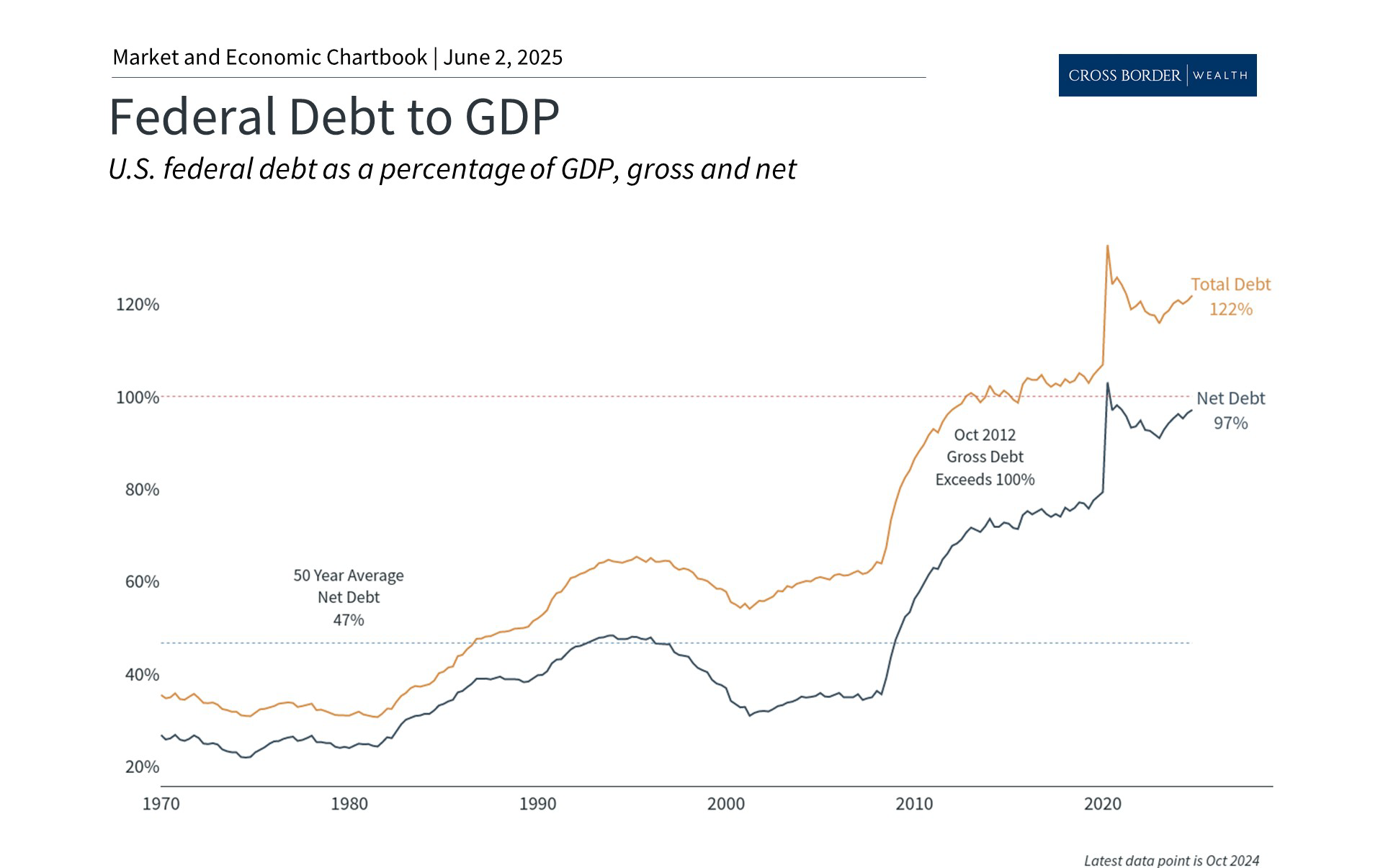

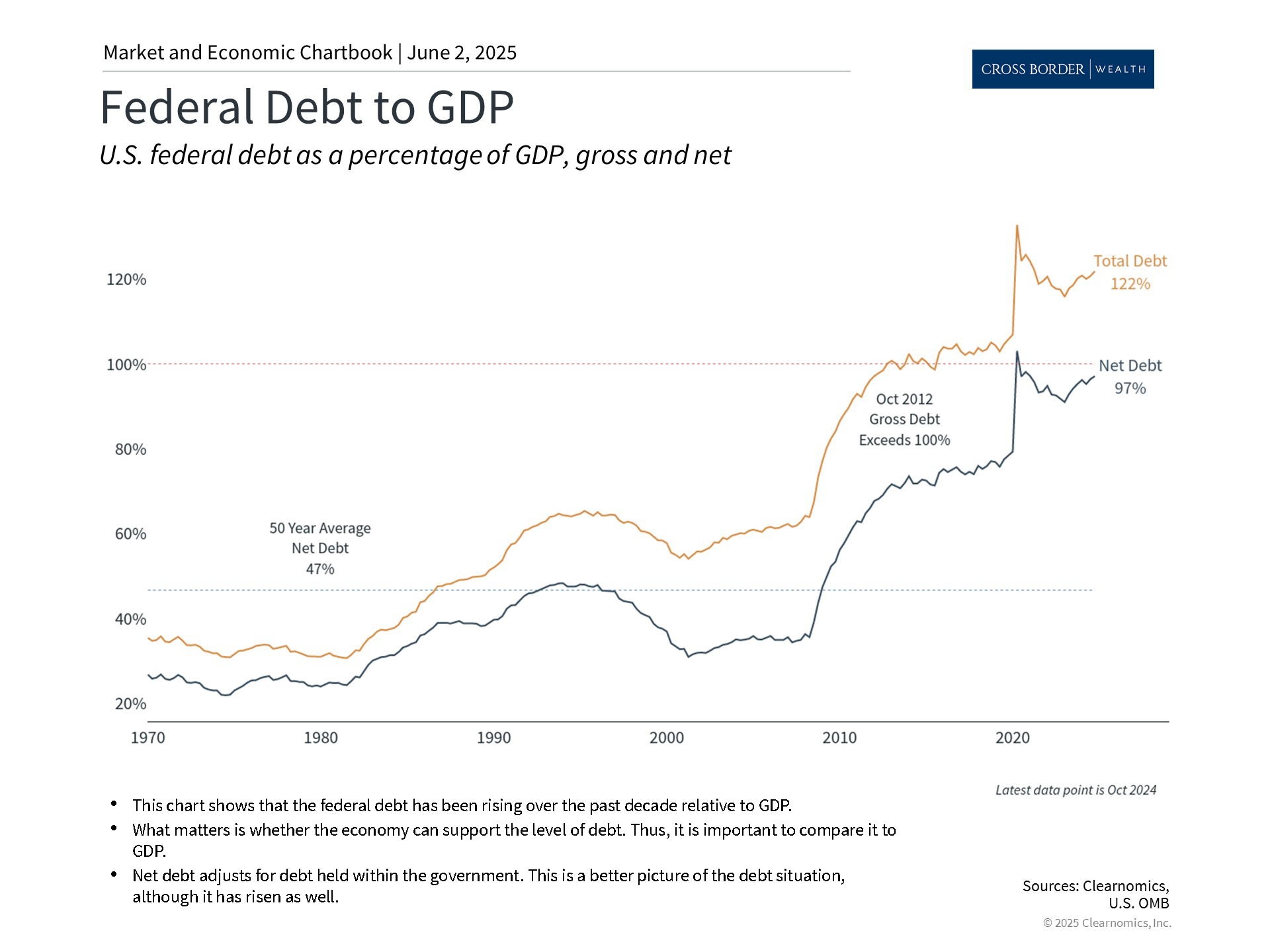

One of the biggest surprises in May was Moody's downgrade of the U.S. credit rating from Aaa to Aa1. This followed previous downgrades by Fitch in 2023 and Standard & Poor's in 2011 which all reflect concerns about the nation's growing debt and spending. The accompanying chart shows that the U.S. total debt grew to 122% of GDP in 2024. Net debt, which excludes debt the government owes itself, has risen to 97%.

Despite the historic nature of the U.S. debt downgrade, markets hardly reacted. This is because the downgrade is mostly backward-looking, and investors are already familiar with the nation's fiscal challenges. The muted response also reflects lessons from the 2011 Standard & Poor’s downgrade, when Treasury securities continued to be viewed as safe haven assets.

Perhaps it was not a coincidence that this downgrade occurred as the House of Representatives was passing a comprehensive tax and spending bill. The approved bill would extend the individual tax cuts from the Tax Cuts and Jobs Act. This includes a 37% top rate, child tax credits, higher State and Local Tax deduction caps, and exemptions for tips and overtime pay, among other measures. According to the Penn Wharton Budget Model, the legislation could increase deficits by $2.8 trillion over the next 10 years.

2 The bill will now be debated and potentially modified in the Senate.

While many would agree that these fiscal challenges require long-term solutions, the U.S. dollar remains the world's primary reserve currency and there will continue to be demand for Treasurys for the foreseeable future.

Trade negotiations show progress

Past performance is not indicative of future results

There was also progress on trade negotiations in May, taking many of the worst-case scenarios off the table. The administration reached agreements with both the U.K. and China, while negotiations continued with other major trading partners. The U.S.-China trade agreement included a 90-day period of reduced U.S. tariffs on Chinese goods.

Despite these deals, there will likely continue to be uncertainty around trade. More recently, China and the U.S. have both accused each other of violating the trade truce, and the administration wants higher tariffs on steel and aluminum. At the same time, negotiations with the European Union produced optimism when the White House delayed its scheduled 50% EU tariff after positive discussions. This suggests that diplomatic solutions remain possible, even when initial positions appear far apart.

The administration is also facing legal challenges to its tariffs. In May, the U.S. Court of International Trade struck down many of the newly enacted tariffs, ruling that they exceed presidential power under the International Economic Emergency Powers Act. While a federal appeals court paused the ruling, allowing tariffs to remain in place for now, this legal challenge adds another layer of uncertainty to the trade landscape.

It is important to remember that trade policy typically unfolds over months and years rather than days or weeks. The recovery in May is a reminder that investors should not overreact to trade headlines, especially now that the worst-case scenarios are less likely to occur.

Steady earnings growth supports market

Past performance is not indicative of future results

First quarter corporate earnings reports presented another reason for optimism. S&P 500 companies delivered positive earnings per share surprises and 64% reported positive revenue surprises, according to FactSet.

3 This strong earnings performance highlighted the underlying health of corporate profitability, with technology companies showing resilience as they navigate trade uncertainty.

In contrast, consumers have been pessimistic this year due to tariffs and inflation concerns. However, recent sentiment indicators began showing signs of improvement that align more closely with positive earnings and economic data. The University of Michigan's most recent survey for May showed inflation expectations decreasing slightly and sentiment stabilizing. While it's important not to read too much into a single month's data, this improvement represents an encouraging development. A strong economy and improving sentiment could help to support markets.

1. Standard & Poor’s, Nasdaq, Bloomberg. All month end figures are as of May 30, 2025.

2. https://budgetmodel.wharton.upenn.edu/issues/2025/5/23/house-reconciliation-bill-budget-economic-and-distributional-effects-may-22-2025

3. FactSet Earnings Insight May 30, 2025