- Market Insights

- 7 mins

Most retirees know that healthcare is often the largest and most unpredictable expense in retirement, which can add up to hundreds of thousands of dollars on average. Healthcare can come from many sources, with Medicare being a major consideration in the financial planning process. Yet, despite its importance, Medicare rules can create confusion for many Americans.

Understanding how Medicare works, the choices it presents, and how those choices affect a broader financial plan is essential for retirees and those approaching retirement. Getting these decisions right can help protect savings, maximize health coverage, and manage cash flow across decades of retirement.

Why Medicare matters today

Medicare was signed into law by President Lyndon B. Johnson on July 30, 1965. It originally consisted of Part A (Hospital Insurance) and Part B (Medical Insurance), together known as Original Medicare. Over the decades, Congress has expanded the program to cover more Americans and offer additional benefits, including prescription drug coverage. Today, Medicare provides health coverage for over 68 million Americans, including approximately 61 million people aged 65 and older and 7 million younger individuals with disabilities.

1

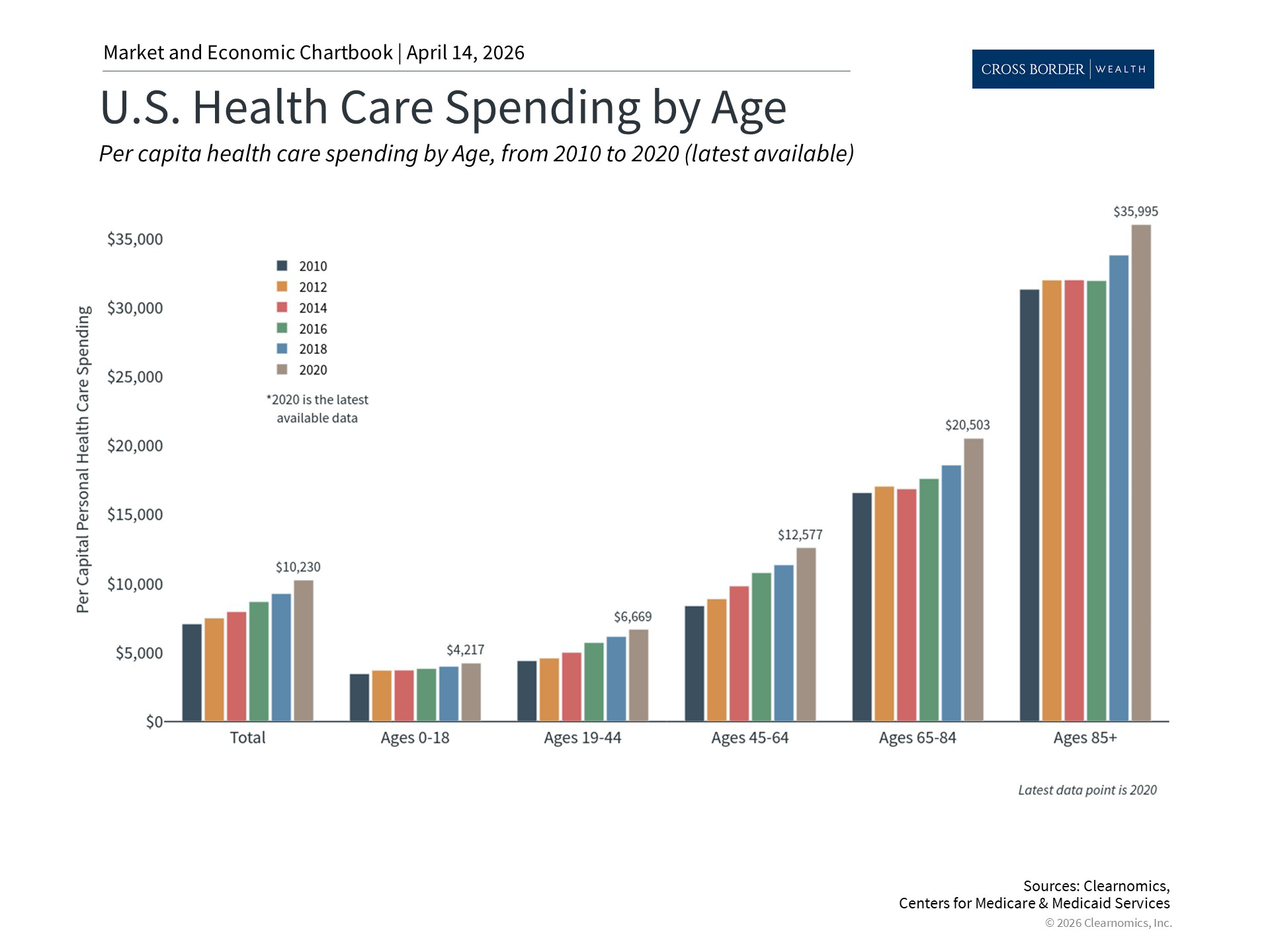

Medicare's importance has only grown as healthcare costs have risen steadily. According to the Centers for Medicare and Medicaid Services, in 2024, national health expenditures grew to roughly $15,474 per person, accounting for 18% of GDP. Over the next decade, healthcare spending is also projected to outpace GDP growth. For retirees, many of whom live on fixed incomes, the program provides essential financial relief against these rising costs.

The program is currently structured into four parts:

• Part A covers inpatient hospital stays, skilled nursing, and hospice care, which is typically premium-free for those who have worked at least ten years.

• Part B covers physicians’ services, outpatient care, and preventive services, requiring a monthly premium that is subject to income-based surcharges.

• Part C, known as Medicare Advantage, is offered by private insurers as an alternative to Original Medicare, and often includes additional benefits such as dental, vision, and hearing coverage.

• Part D provides optional prescription drug coverage through private insurers and is also subject to income-based surcharges.

A common misconception is that Medicare is free because individuals have contributed through payroll deductions for years. While Part A is indeed covered for most people, Part B premiums, supplemental coverage, and out-of-pocket costs can add up significantly. This is why integrating Medicare decisions into a comprehensive financial plan is so important.

The Medicare income cliff: Why IRMAA planning matters

Past performance is not indicative of future results

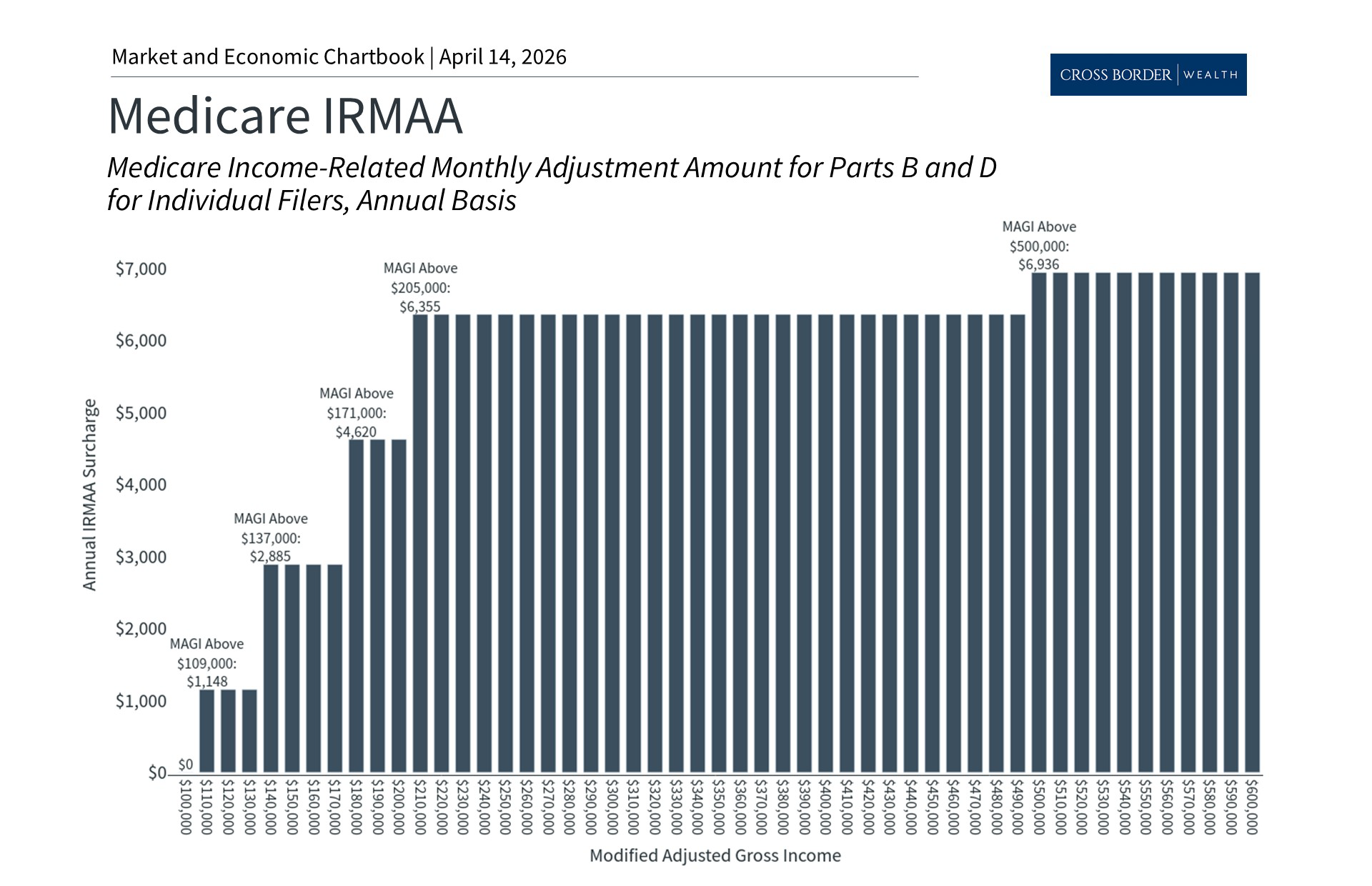

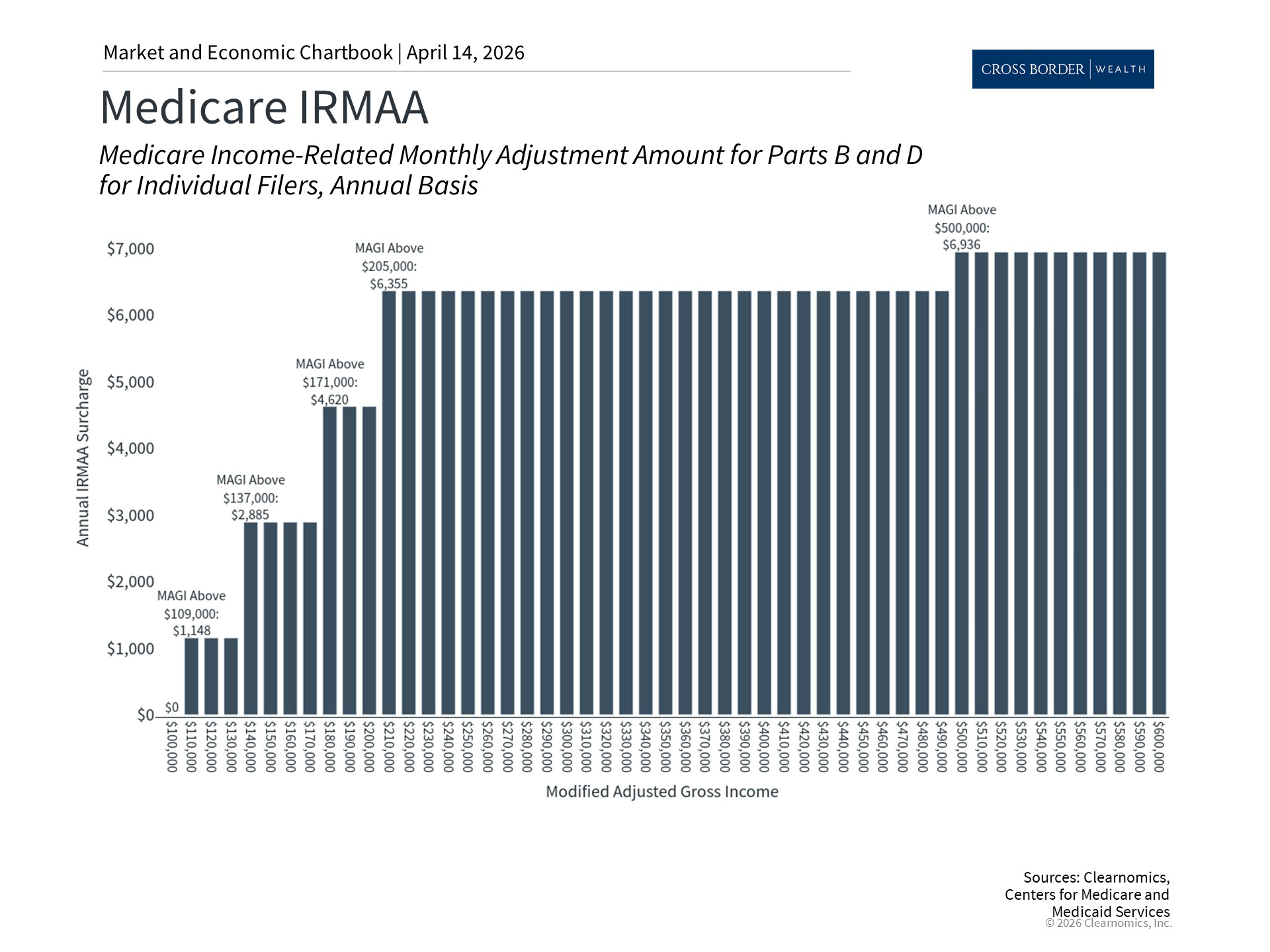

One of the biggest Medicare surprises that catches retirees off guard is IRMAA. This is an extra charge added to Medicare premiums which kicks in if you earn more than $109,000 as an individual or $218,000 as a married couple filing jointly. These amounts are for coverage year 2026 and are adjusted annually.

IRMAA stands for Income-Related Monthly Adjustment Amount and it affects Medicare Part B and Part D premiums. Unlike the marginal tax brackets that many taxpayers are used to, where only the income above each threshold is taxed at a higher rate, IRMAA operates as a cliff. This means that if your income exceeds a threshold by even one dollar, you pay the full surcharge for that entire bracket. This can catch even savvy retirees by surprise if their income rises above certain levels.

What makes this even trickier is that IRMAA is applied each year based on your Modified Adjusted Gross Income (MAGI) from two years prior, since that would be the latest tax filing available. So, for instance, the surcharge you face at age 65 is determined by your income in the calendar year you turned 63. This two-year lookback means that financial decisions made years before Medicare enrollment, such as Roth conversions, capital gains realizations, or even the timing of Social Security benefits, can have consequences.

It's also important to understand that the income thresholds for IRMAA and for IRS marginal tax brackets are different. A common strategy when tax planning is to "fill up" a tax bracket by recognizing additional income, such as Roth conversions. However, doing so without considering IRMAA thresholds can inadvertently push you over a cliff, resulting in hundreds or even thousands of dollars in additional annual premiums.

There are several strategies that can help manage IRMAA exposure. Qualified Charitable Distributions, for example, allow retirees to direct Required Minimum Distributions to charity without increasing their Adjusted Gross Income, unlike standard charitable deductions which reduce taxes but don't lower MAGI. Timing Roth conversions at least two years before Medicare enrollment can also help, since that income will be reflected in the lookback period before surcharges apply.

Delaying Social Security is another consideration that cuts both ways. While it reduces current income and can help avoid IRMAA thresholds in the near term, the higher payments that result from delaying could coincide with Required Minimum Distributions later, potentially pushing income above surcharge levels in future years. These trade-offs are exactly why income planning in retirement requires a coordinated, multi-year approach.

Medigap vs. Medicare Advantage

Past performance is not indicative of future results

Beyond income planning, another consequential decision retirees face is choosing between Medigap (also known as Medicare Supplement Insurance) and Medicare Advantage. This choice is not just affected by an individual’s healthcare coverage requirements, but also the financial risk profile of their retirement plan. From a financial planning perspective, this choice comes down to risk tolerance, lifestyle choices, and predictability.

Medigap complements Original Medicare (Parts A and B) to help cover out-of-pocket costs such as deductibles, coinsurance, and copayments. Premiums are higher, ranging from roughly $32 to $550 per month depending on the plan and location, but out-of-pocket costs are lower and more predictable.

Medicare Advantage, on the other hand, can act as a comprehensive alternative to Original Medicare. These plans are offered by private insurers and often include dental, vision, and hearing benefits. Premiums are frequently low, making them attractive at first glance. However, they typically come with higher out-of-pocket costs with annual expense caps, network restrictions, and certain referral requirements that may result in denied care. Trade-offs need to be considered including the potential inability to switch back to a Medicare Supplemental plan later on due to medical underwriting.

Medigap offers higher fixed costs with more predictable total expenses, similar to paying a higher insurance premium for more comprehensive coverage. It also offers nationwide coverage–an important consideration for retirees who expect to travel often. Medicare Advantage offers lower upfront costs but introduces more variability in annual healthcare spending, especially for those with chronic conditions or unexpected medical needs.

For retirees with substantial Health Savings Account balances or other dedicated healthcare funds, the variable costs of Medicare Advantage may be manageable. For those who prioritize budget certainty or who have health conditions requiring frequent care, Medigap's predictability may be worth the higher premium. In 2025, the average beneficiary had 42 Medicare Advantage plans to choose from, which underscores how important it is to evaluate options carefully each year.

Monitoring personal circumstances and policy updates

Medicare planning is not a one-time decision. It requires annual review because available plans, premiums, health status, and income levels can all change from year to year. It is also important to monitor any policy changes, such as IRMAA thresholds or definitions. Unlike more predictable financial goals such as saving for education, healthcare expenses are variable and tend to increase with age, making ongoing adjustments an essential part of any retirement plan.

Additional considerations to keep in mind:

• Timing is critical.

Missing the Initial Enrollment Period, which is a seven-month window centered around one’s 65th birthday, can result in a permanent 10% penalty on Part B premiums for every year delayed, unless individuals qualify for a Special Enrollment Period through active employment.

• Limited long-term care coverage.

One fact that surprises some is that Medicare provides only limited long-term care support under specific circumstances, such as a qualifying hospital stay and admission to a Medicare-approved skilled nursing facility for a condition expected to improve.

• Life events can impact costs.

Major life changes, such as job loss, divorce, or the death of a spouse, can trigger a reassessment of IRMAA surcharges, potentially lowering premiums if income declines.

If you navigate Medicare well, it can support a more secure and predictable retirement. The key is proactive planning by making sure you understand how to navigate the complexities ahead of time.

Need tailored cross-border solutions?

Consult with one of our cross-border advisors.

What to Expect in the Consultation

- Discuss your circumstance with a cross-border advisor

- Identify costly pitfalls faced by US-connected expats

- Understand compliance and reporting regulations

- Gain clarity on complex international tax treaties

- Know your available options and next steps

References

1. https://data.cms.gov/summary-statistics-on-beneficiary-enrollment/medicare-and-medicaid-reports/medicare-monthly-enrollment